Gold is a commodity that is often bought as a store of wealth to protect against severe market dislocation. With the S&P 500 Index near record highs and at historically extreme valuation levels, it makes sense that investors have been investing in the yellow metal. However, with gold up around 20% over the past year and many gold miners up far more than that, is now a good time to jump aboard? The answer isn't easy, but here are some thoughts to help you make the right call for your portfolio -- and three stocks that you'll want to get to know a little better.

What goes up...

Gold is a commodity that's subject to the whims of investor sentiment. While supply and demand do play roles, right now fear and greed are the more important factors. If you are afraid of a market downturn, buying gold is a logical choice, as long as you don't go overboard. Maybe 10% of your assets would be an appropriate target to get the diversification benefits the metal can offer.

Image source: Getty Images

However, buying physical gold isn't the best choice because of transaction costs and storage concerns. An exchange traded fund (ETF) that owns physical gold, like SPDR Gold Shares (NYSEMKT: GLD), would be a better alternative. However, both of these options suffer from one key drawback: Physical gold has no growth potential beyond price changes -- an ounce of gold will always be an ounce of gold. Gold miners, on the other hand, can expand their production. So they provide exposure to gold and a chance for long-term growth as they increase the size and scale of their businesses.

But even here there's a better option: gold streaming companies. To simplify the model, companies like Royal Gold (NASDAQ: RGLD), Wheaton Precious Metals (NYSE: WPM), and Franco-Nevada (NYSE: FNV) provide cash up front to miners for the right to buy gold, and other metals, at reduced rates in the future. The miners get access to cash for expansion projects, new mines, or debt reduction, without having to issue debt or stock, or deal with a bank. The streamers tie up some cash (generally generated from the issuance of stock), but then get a long "stream" of low-cost precious metals that help to keep margins high in good markets and bad. It's pretty close to a win/win in most situations.

The margin issue is important. Falling gold prices will narrow a streamer's margins, since they basically have low purchase prices all the time. But weak precious metals markets can easily push a miner into the red. Worse, a miner facing low prices usually has to adjust operations if they want to cut costs to protect margins. That takes time and usually comes with its own costs, burdening margins even further over short periods. The streaming model is much more resilient in the face of adversity.

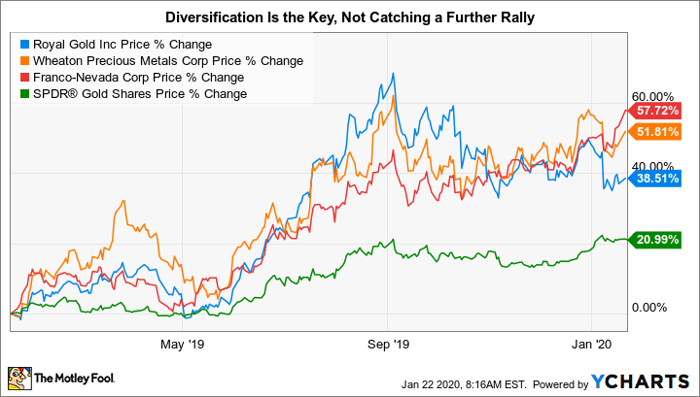

All in all, if you are worried about the elevated level of the market today, putting a little of your portfolio into a streaming company would be a reasonable way to diversify. That remains true even though Royal Gold's stock is up 38% over the past year, with Wheaton and Franco-Nevada up 51% and 57%, respectively. Just go in knowing that diversification is the goal, rather than thinking you're jumping on a hot stock. These companies could easily give up some of their gains. Royal Gold, for example, is off around 17% from the highs it reached in September. Wheaton is off its high by around 6%. Only Franco-Nevada is still trading near all-time highs. Which highlights this caveat: If your goal is really to avoid all risk, then the best option is cash.

Which one is right for you?

Assuming that you want to remain invested in the stock market and add a little exposure to a company that's tied to gold, then you should dig into the streamers. Royal Gold is the most tightly focused on gold, with around 90% of its revenue tied to precious metals (copper makes up most of the rest) and the vast majority of that (around 80%) linked to gold. Wheaton's revenue is fairly evenly divided between gold and silver, with a relatively small amount of other precious metals starting to show up in the mix.

Franco-Nevada is the most diversified, with about 85% of its revenue tied to precious metals (mostly gold) and then a growing portfolio of oil "streaming" deals (about 15% of revenue). If you are looking for a streaming company that's heavy on gold, Royal Gold is the clear winner. If you are happy just sticking to precious metals, then Wheaton is an option. But if you like the idea of diversification, then Franco-Nevada's energy push could give it the edge. Just go in knowing that it is the furthest away from a pure play here.

These three companies also go about their businesses in very different manners. Wheaton tends to focus on a smaller number of large deals. Its portfolio contains streams from 20 operating mines and investments in nine development projects. Royal Gold's portfolio is far larger, with 186 properties, 41 of which are producing while the rest are in some earlier stage of exploration and development. The company is basically taking more swings in the hope that it can get more hits. Wheaton is looking for home runs.

Franco-Nevada, meanwhile, is by far the most diversified with 296 mining investments. Fifty-six of those are producing, with the rest in an earlier stage of exploration and development. It is, like Royal Gold, taking a lot of swings in the hopes of getting a lot of hits. But it also has a collection of 81 energy investments, 56 of which are producing. It's more like Bo Jackson or Deion Sanders, two baseball players who also had professional football careers. Or, putting aside the sports analogies, you could simply say that Franco-Nevada is diversified in a way that neither of its two main competitors can match.

Dividends are another issue that investors will want to look at. Although none of these companies has a particularly large yield, they all make a point of returning cash to investors (Wheaton, for reference, tops the list with a 1.3% dividend yield.) Royal Gold and Franco-Nevada both have long histories of regular annual dividend increases, at 19 years and 12 years, respectively. Note that Franco-Nevada hasn't been public as long as Royal Gold, so you shouldn't view the shorter history as a negative.

Wheaton's dividend, meanwhile, is tied to its operating performance, so its payment will go up and down over time. Although that could be seen as a negative, the dividend will tend to increase when precious metal prices are high. That is likely to correspond to periods when stock markets are facing headwinds and other investments you own might be at risk of cutting dividends. So the dividend might actually go up right when you most want it to, helping to offset dividend challenges in the rest of your portfolio. That said, if income consistency is important to you, than Wheaton is best avoided.

The last issue to consider is growth potential. Streaming has gone through a number of growth phases. Right now, large gold miners are in relatively good shape, and consolidation is the big industry story. But as big miners pair up, they are selling smaller assets and those that don't fit well with their broader portfolios. Streamers are hoping that they can help with the process by assisting those that may be interested in taking on the properties that merging miners want to unload. This, however, would appear to favor Royal Gold and Franco-Nevada, since smaller assets are more likely to be jettisoned than the larger mines Wheaton is focused on. That said, Wheaton has some sizable projects it's funding, so it isn't going to fall flat. Just don't go in expecting it to make a lot of big growth-enhancing deals, even if its peers are happily writing a lot of checks.

Buying gold the right way

If you are worried by the lofty valuations in the stock market today, than gold might be an enticing asset class to include in your portfolio to enhance your overall diversification. Buying gold, however, probably isn't the best approach. Instead, take a serious look at streamers like Royal Gold, Wheaton, and Franco-Nevada. Their stocks are up a lot over the past year, but they have attractive business models and still offer enticing opportunities today. Of the trio, Royal Gold is most tightly tied to the yellow metal, and Franco-Nevada is the most diversified.

10 stocks we like better than Royal Gold

When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the ten best stocks for investors to buy right now... and Royal Gold wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of December 1, 2019

Reuben Gregg Brewer owns shares of Franco-Nevada. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

"much" - Google News

January 27, 2020 at 12:23AM

https://ift.tt/2RQlS1L

Up as Much as 57% in a Year, Are These Gold Stocks Still Buys? - Nasdaq

"much" - Google News

https://ift.tt/37eLLij

Shoes Man Tutorial

Pos News Update

Meme Update

Korean Entertainment News

Japan News Update

Bagikan Berita Ini

0 Response to "Up as Much as 57% in a Year, Are These Gold Stocks Still Buys? - Nasdaq"

Post a Comment